Monetary Policy Tools

The secret levers that shape economies and your wallet! 💰✨

Featured partners and sponsors

New advertisers get $25 in ad credits

Monetary policy tools | Financial sector | AP Macroeconomics | Khan Academy

⚡ THE VIBE

✨Monetary policy tools are the powerful instruments central banks wield to manage a nation's money supply, credit conditions, and interest rates, fundamentally shaping economic growth, inflation, and employment. Think of them as the levers and dials on a sophisticated economic control panel! 🕹️

§1The Maestro's Orchestra: What Are They?

Imagine the economy as a vast, intricate orchestra 🎻, and the central bank as its maestro. Monetary policy tools are the conductor's baton, allowing them to speed up, slow down, or fine-tune the economic rhythm. At their core, these tools aim to manage the money supply – the total amount of currency in circulation and available credit – to achieve macroeconomic goals like price stability (keeping inflation in check), maximum sustainable employment, and moderate long-term interest rates. It's a delicate balancing act, often likened to steering a supertanker: subtle adjustments are required, and the effects aren't always immediate. 🚢

§2A Brief History of Economic Levers 🕰️

While central banking itself has roots stretching back centuries, the systematic application of monetary policy tools as we know them largely solidified in the 20th century, particularly with the establishment of institutions like the Federal Reserve in 1913. Initially, the primary tool was the discount rate, influencing how much commercial banks paid to borrow from the central bank. Over time, open market operations (buying and selling government securities) became the dominant mechanism. The 2008 financial crisis and the subsequent 'Great Recession' ushered in an era of unconventional tools like quantitative easing (QE), proving that even the most established playbooks can be expanded when the economic stakes are sky-high. 🚀

§3The Core Toolkit: How Central Banks Operate 🛠️

Central banks primarily rely on a few key instruments to achieve their objectives. Understanding these is crucial to grasping global economic shifts:

- Interest Rates (Policy Rate): This is often the headline-grabber! The central bank sets a target for a key short-term interest rate (e.g., the federal funds rate in the US). By influencing this rate, they affect borrowing costs across the entire economy. Lower rates encourage borrowing and spending 💰; higher rates curb inflation by making money more expensive. It's their most direct signal to the market.

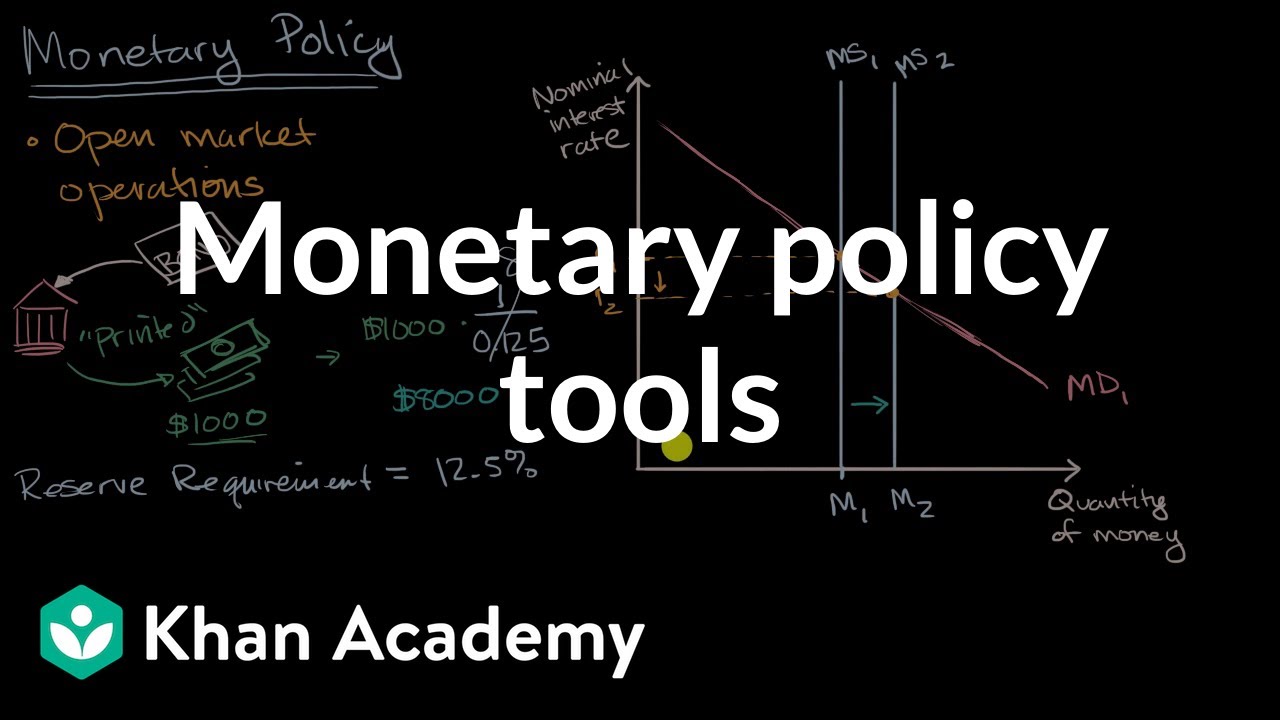

- Open Market Operations (OMOs): This is the central bank's daily bread and butter. They buy or sell government securities (like Treasury bonds) in the open market. Buying securities injects money into the banking system, increasing reserves and lowering interest rates. Selling securities removes money, tightening credit and raising rates. It's a precise way to manage liquidity. 💧

- Reserve Requirements: This dictates the minimum fraction of customer deposits that commercial banks must hold in reserve, rather than lend out. Lowering requirements frees up more money for lending, while raising them restricts it. While historically significant, many central banks (like the Fed since 2020) have reduced or eliminated reserve requirements, relying more on interest rates and OMOs. 🏦

- Discount Window Lending: This is the central bank's role as 'lender of last resort.' Banks can borrow directly from the central bank at the 'discount rate' to meet short-term liquidity needs. While less frequently used for routine policy, it's a critical safety net during financial stress. 🛡️

§4Beyond the Basics: Unconventional Tools & Future Trends 💡

When traditional tools aren't enough, especially during severe economic downturns or periods of very low interest rates (the dreaded 'zero lower bound'), central banks turn to unconventional measures. Quantitative Easing (QE), for example, involves massive purchases of longer-term government bonds and other assets to directly lower long-term interest rates and inject liquidity. Other strategies include forward guidance (communicating future policy intentions to influence expectations) and negative interest rates (where banks pay to hold reserves at the central bank, pushing them to lend). The 2020s have seen central banks navigating new challenges, from supply chain shocks to climate change considerations, hinting at an ever-evolving toolkit. The future might even see central banks exploring Central Bank Digital Currencies (CBDCs) as a new monetary policy lever! 🌐

§5Why It Matters: Your Wallet, Your Job, Your Future 🌍

Understanding monetary policy isn't just for economists in ivory towers; it impacts everyone. The decisions made by central banks directly influence:

- The interest rate on your mortgage 🏡 and car loan 🚗.

- The returns on your savings account 💰.

- The overall cost of living (inflation) 📈.

- The availability of jobs and economic growth 🧑💼.

When central banks get it right, the economy hums along, stable and growing. When they misstep, the consequences can be severe, leading to recessions, high inflation, or even financial crises. It's a constant, high-stakes game of economic engineering, shaping the financial landscape we all live in. So next time you hear about interest rate decisions, know that it's more than just a number – it's a fundamental force shaping our world! ✨