Summary

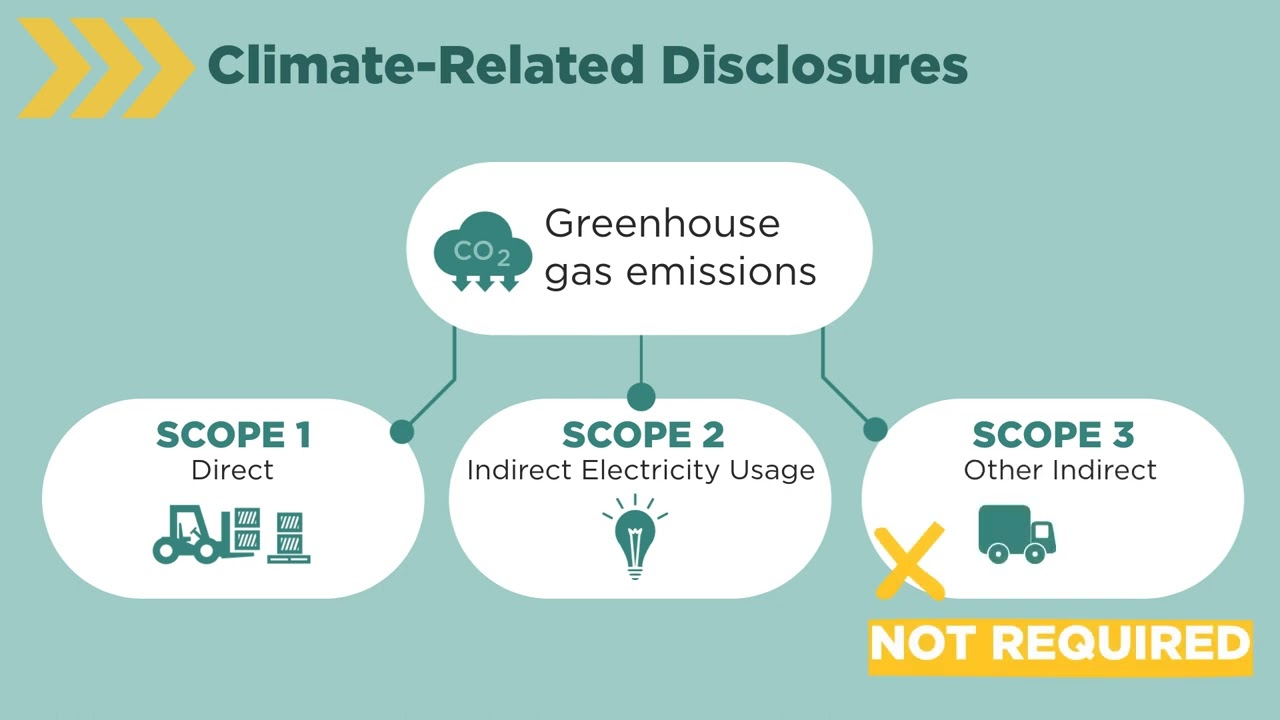

**SEC** has finalized rules requiring public companies to disclose climate-related risks and financial impacts, marking a major shift in corporate accountability. The rules mandate **material climate risk disclosures** in SEC filings, including Scope 1/2 emissions, mitigation strategies, and board oversight [[~climate-disclosure-rules|Climate Disclosure Rules]]. This follows a 2021 SEC proposal and aligns with global standards like the **TCFD** [[~task-force-on-climate-related-financial-disclosures|TCFD]]. The move responds to investor demand for standardized data, but critics warn of compliance costs and potential greenwashing [[~greenwashing|Greenwashing]]. The rules require companies to detail **climate-related financial impacts**, **mitigation expenditures**, and **board oversight processes**. Large accelerated filers must disclose Scope 1/2 emissions, while all companies must report on **transition plans** and **scenario analysis**. This creates a **new baseline for ESG investing** [[~esg-investing|ESG Investing]] and could reshape **corporate governance** [[~corporate-governance|Corporate Governance]] frameworks. The SEC claims this will provide **'decision-useful information'** for investors, but skeptics question whether the rules will actually reduce systemic climate risks or merely shift reporting burdens.

Key Takeaways

- SEC mandates climate risk disclosures in SEC filings for all public companies

- Rules require Scope 1/2 emissions reporting for large accelerated filers

- Disclosures must include board oversight and mitigation strategies

- The rules aim to standardize climate data for investor decision-making

- Uncertainties remain about compliance costs and effectiveness

Balanced Perspective

The SEC's rules **standardize climate disclosures** as requested by investors, but the **cost-benefit balance remains unclear**. While the rules provide **consistent reporting**, they may **increase compliance burdens** for smaller firms. The **definition of 'material' climate risks** is subjective, leaving room for **interpretive flexibility**. The **requirement to report Scope 1/2 emissions** could **pressure fossil fuel firms** to disclose carbon footprints, but **lack of enforcement mechanisms** raises questions about **adherence rates**. The **SEC's emphasis on 'truthful disclosure'** aligns with its mandate, but **long-term impact on corporate behavior** remains to be seen.

Optimistic View

**Investors gain actionable data** to assess climate risks, enabling smarter portfolio decisions. Standardized disclosures will **reduce information asymmetry** and **lower systemic risk** by forcing companies to quantify climate impacts. The rules **align U.S. standards with global norms** like the TCFD, enhancing **international investor confidence**. By mandating **board-level oversight**, the SEC is pushing firms to integrate climate risk into **strategic planning** [[~strategic-planning|Strategic Planning]]. This could **accelerate the transition to sustainable business models** and **drive innovation in clean tech**.

Critical View

The rules risk **creating regulatory complexity** without clear **performance metrics** to measure success. **Smaller companies** may struggle with **compliance costs**, potentially **skewing market access** toward larger firms. The **focus on financial impacts** may **understate systemic climate risks** like biodiversity loss or geopolitical instability. **Greenwashing** could persist if companies **overstate mitigation efforts** or **underreport Scope 3 emissions** [[~scope-3-emissions|Scope 3 Emissions]]. The **SEC's own climate risk exposure** [[~sec-climate-risk|SEC Climate Risk]] highlights the **irony of regulating climate risk without internal safeguards**.

Source

Originally reported by sec.gov