Contents

Overview

The lack of health insurance refers to the condition of an individual or population segment not having any form of health coverage, leaving them financially exposed to medical expenses. This absence can stem from various factors, including inability to afford premiums, ineligibility for employer-sponsored plans, or gaps in government programs. Globally, hundreds of millions remain uninsured, with significant disparities across countries and within them. In the United States, for instance, despite being a wealthy nation, a substantial portion of the population has historically navigated this precarious situation, leading to delayed care, medical debt, and poorer health outcomes. The issue is a complex interplay of economic, social, and political forces, constantly debated and reshaped by policy interventions and market dynamics.

🎵 Origins & History

The concept of being uninsured isn't new, but its modern manifestation is deeply tied to the rise of industrialization and the subsequent development of formal healthcare systems. Historically, communities relied on informal networks, religious charities, or personal savings to manage illness. The formalization of health insurance as a mechanism to pool risk began in earnest in the late 19th and early 20th centuries. In the United States, the absence of a robust, government-mandated system has perpetuated a significant uninsured population throughout the 20th and into the 21st century.

⚙️ How It Works

At its core, health insurance functions as a risk-pooling mechanism. Individuals or groups pay regular premiums to an insurance company or government program. In return, the insurer agrees to cover a portion of the policyholder's medical costs, typically above a deductible and up to an annual or lifetime maximum. When an individual lacks insurance, they are directly responsible for the full cost of any medical services they receive. This can range from routine doctor's visits and prescription drugs to emergency room care and complex surgeries. Without insurance, the financial burden of unexpected illness or injury can be catastrophic, leading to significant debt or forcing individuals to forgo necessary medical treatment altogether, a phenomenon often referred to as 'underinsurance' when coverage is insufficient.

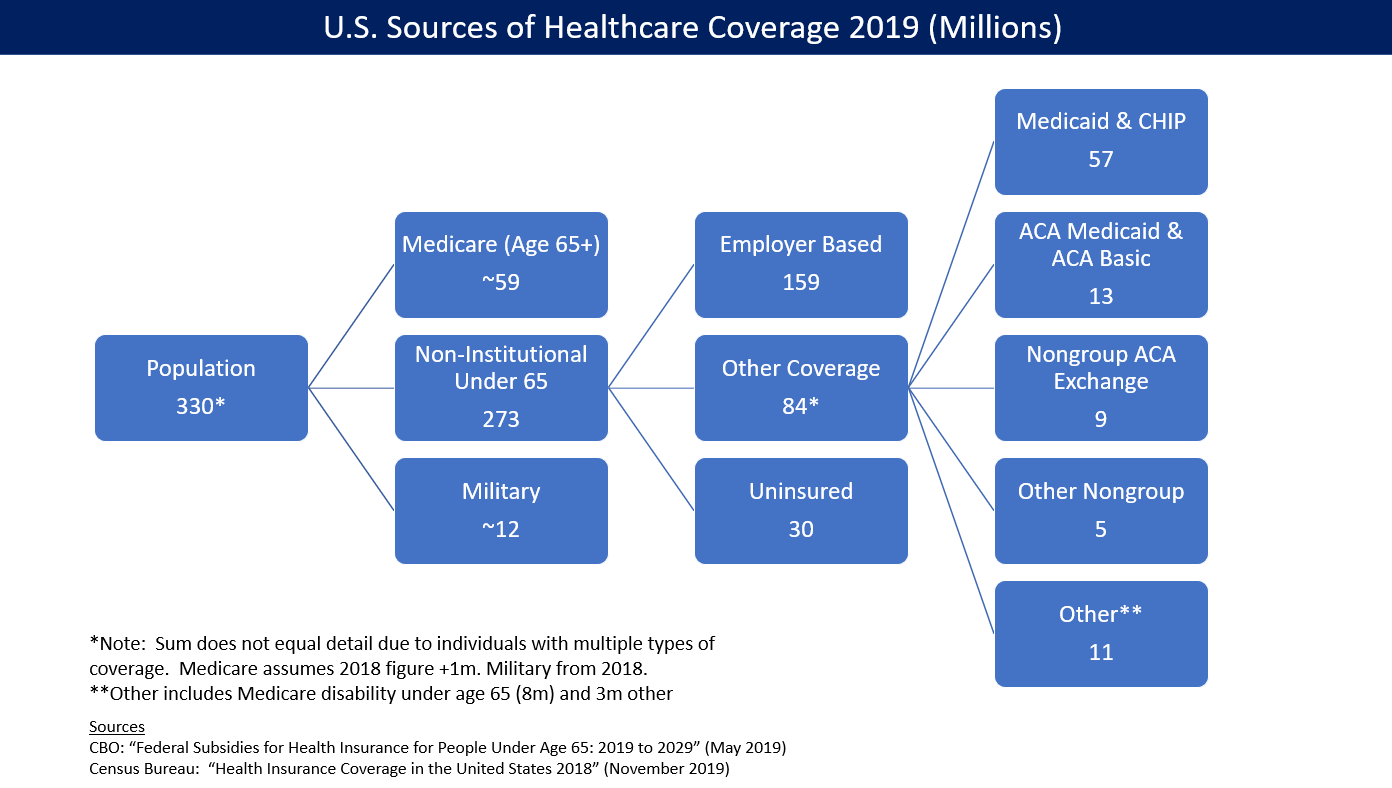

📊 Key Facts & Numbers

Globally, the scale of uninsurance is staggering. In the United States, while the Affordable Care Act (ACA) (passed in 2010) significantly reduced the uninsured rate, approximately 26 million Americans remained uninsured in 2022, according to Kaiser Family Foundation data. This figure represents about 8% of the total U.S. population. For children, the uninsured rate was even lower, around 5% in 2022, thanks to programs like Medicaid and the Children's Health Insurance Program (CHIP). However, millions still fall into coverage gaps, particularly in states that did not expand Medicaid.

👥 Key People & Organizations

Key figures and organizations have shaped the discourse and policy surrounding health insurance. President Barack Obama championed the Affordable Care Act (ACA), aiming to expand coverage through marketplaces and Medicaid expansion. Organizations like the Kaiser Family Foundation and the American Medical Association (AMA) are significant players in research, advocacy, and policy analysis. Think tanks such as the Heritage Foundation and the Brookings Institution often present contrasting viewpoints on healthcare reform.

🌍 Cultural Impact & Influence

The lack of health insurance casts a long shadow over individual lives and societal well-being. It's a potent symbol of economic insecurity and a driver of health disparities. For individuals, it can mean delaying or foregoing necessary medical care, leading to worse health outcomes and increased mortality rates. The fear of medical bankruptcy is a pervasive anxiety for many uninsured and underinsured individuals, impacting their financial planning and overall quality of life. Culturally, it fuels debates about fairness, individual responsibility versus collective well-being, and the role of government in ensuring basic human needs. The visibility of this issue in media and political discourse underscores its deep resonance within societies that grapple with healthcare access.

⚡ Current State & Latest Developments

As of 2024, the landscape of health insurance remains dynamic. In the United States, efforts to repeal and replace the Affordable Care Act continue to surface, creating uncertainty for millions. Some states have pursued further Medicaid expansion, while others have resisted. The rise of high-deductible health plans (HDHPs) has also led to concerns about underinsurance, where individuals have coverage but still face significant out-of-pocket costs. Globally, many developing nations are striving to expand their health coverage through initiatives like universal health coverage (UHC) schemes, often supported by international bodies like the World Bank and the WHO. The ongoing COVID-19 pandemic highlighted the critical importance of health insurance for accessing testing, treatment, and vaccines, further intensifying discussions around coverage gaps.

🤔 Controversies & Debates

The debate surrounding the lack of health insurance is multifaceted and often polarized. Critics of government-mandated insurance argue that they stifle innovation, lead to long wait times, and represent an overreach of government power, infringing on individual liberty and free market principles. Proponents, conversely, contend that healthcare is a fundamental human right and that a lack of insurance creates unacceptable health disparities and economic burdens on society. Arguments often center on the economic efficiency of different models, the ethical implications of denying care, and the role of private versus public entities in healthcare provision. The concept of 'moral hazard' – that insured individuals might overuse services – is frequently debated against the 'adverse selection' problem, where only the sickest seek insurance, driving up costs.

🔮 Future Outlook & Predictions

The future outlook for addressing the lack of health insurance is uncertain but points towards continued policy evolution. In the U.S., potential pathways include further strengthening the ACA, exploring public option insurance plans, or more significant reforms towards a single-payer system like Medicare for All. Internationally, the push for universal health coverage is expected to continue, with many nations focusing on primary care access and financial protection. Technological advancements, such as telehealth and AI-driven diagnostics, may also play a role in reducing costs and improving access, though ensuring equitable distribution of these benefits remains a challenge. The long-term trend suggests a global movement towards greater health coverage, but the pace and form it takes will vary significantly.

💡 Practical Applications

For individuals facing a lack of health insurance, practical applications revolve around navigating available resources and mitigating financial risk. This includes exploring eligibility for government programs like Medicaid, Medicare, or CHIP, and investigating options on the ACA marketplaces, which may offer subsidies. Community health centers and Planned Parenthood clinics often provide affordable care regardless of insurance status. For those with high-deductible plans, understanding preventative care benefits and utilizing health savings accounts (HSAs) can be crucial. In emergencies, understanding hospital EMTALA obligations (in the US) can clarify rights regarding stabilization. Many non-profit organizations also offer assistance programs for specific conditions or populations.

Key Facts

- Category

- vibes

- Type

- topic